Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer.

Slippage is the gap between the price you expected and the price you actually got. You see BTC at $100,000, hit buy, and fill at $100,050 — that $50 is slippage. It seems minor, but for active traders and bots it's a persistent drag on returns, and in volatile or illiquid conditions it can be severe. This guide explains what causes slippage, when it's worst, and the practical ways to minimize it.

Slippage is closely tied to the order book and liquidity concepts — if you've read those guides, this will click quickly. It's a cost you can't eliminate but can substantially control.

TL;DR — The 30-second answer

- Slippage is the difference between your expected price and your actual fill price.

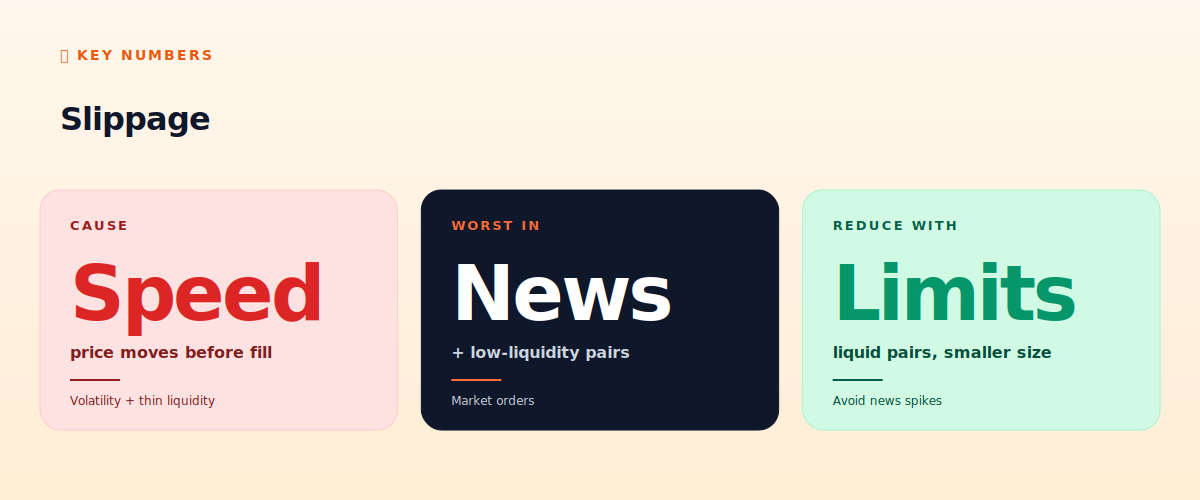

- Cause: price moves (or the order book shifts) between your decision and execution.

- Worst in: volatile conditions, thin liquidity, large orders, and around news.

- Market orders suffer slippage; limit orders avoid it (but may not fill).

- Minimize with: liquid pairs, smaller orders, limit orders, avoiding news spikes.

- For bots, slippage is a real cost that erodes thin-edge strategies.

What slippage looks like

What causes slippage

Slippage happens because there's a tiny delay between deciding to trade and the trade executing, and because of how orders fill against the order book. Two mechanisms:

- Price movement during the delay: in the milliseconds between you (or your bot) submitting an order and it executing, the price can move. In fast markets, the price you saw is already gone.

- Walking the book: a market order larger than what's available at the best price fills the best level, then the next, then the next — each at a worse price. Your average fill is worse than the top-of-book price you saw. This is slippage from consuming depth.

Both mean you get a different (usually worse) price than expected. Slippage can occasionally be positive (you get a better price), but on average and especially in adverse conditions, it works against you.

When slippage is worst

Slippage isn't constant — it spikes under specific conditions:

- High volatility: when price is moving fast, the gap between decision and execution costs more. Crashes and spikes produce severe slippage.

- Thin liquidity: illiquid pairs with shallow order books mean even small orders walk through multiple levels. Obscure tokens and small exchanges are slippage-prone.

- Large orders: the bigger your order relative to available liquidity, the more book levels it consumes, the worse the average fill.

- Around news: high-impact economic releases (see our economic calendar guide) cause both volatility and temporary liquidity gaps — a perfect storm for slippage. Stops can be 'gapped' past entirely.

The worst slippage combines these: a large market order on an illiquid pair during a news-driven volatility spike can fill catastrophically far from the expected price.

Why it matters for bots

For automated and active trading, slippage is a persistent, often-underestimated cost. A backtest that assumes perfect fills at the displayed price will overstate returns — real execution suffers slippage the backtest ignored (a key point in our backtesting guide). For strategies with a thin per-trade edge (scalping, arbitrage, grid), slippage can consume the entire edge — you make the 'right' trades but lose to execution costs. This is part of why triangular arbitrage fails for retail and why scalping is so hard. Any active strategy must account for realistic slippage, not idealized fills.

How to minimize slippage

- Use limit orders. A limit order fills only at your price or better, so it can't slip to a worse price (the trade-off: it may not fill). This is the most direct slippage control — see our order types guide.

- Trade liquid pairs. Deep order books absorb your orders with minimal price movement. Stick to major pairs on large exchanges for size.

- Keep orders reasonably sized. Don't place orders larger than the book can comfortably absorb. Split large orders into smaller pieces over time if needed.

- Avoid trading during news spikes. Step aside around high-impact releases when slippage is worst.

- Set slippage tolerance (on DEXs and some platforms): a maximum slippage you'll accept, beyond which the order cancels rather than fills at a terrible price.

- Be cautious with stops in fast markets. A stop-market order guarantees execution but not price — in a gap, it can fill far from your stop level. Know this risk.

The stop-loss slippage trap

One important nuance: your stop-loss can slip too. A stop-market order triggers and becomes a market order — which means in a fast crash, it can fill well below your stop price. You set a stop at $95,000 expecting to lose a defined amount, but in a violent drop it fills at $93,000, costing more than planned. This is unavoidable with stop-market orders in gapping markets (a stop-limit avoids the bad price but risks not filling at all — arguably worse). It's a reason to size positions conservatively: assume your stop might slip in the worst conditions, and don't risk so much that a slipped stop is catastrophic.

The honest verdict

Slippage is an unavoidable cost of trading that you can substantially control but never fully eliminate. It's worst exactly when you're most vulnerable — volatile markets, thin liquidity, large orders, news events — and it quietly erodes returns, especially for active bots whose backtests assumed perfect fills. Minimize it with limit orders, liquid pairs, sensible order sizing, and news avoidance. Respect that even your stop-loss can slip in fast markets, and size accordingly. Slippage won't make headlines like a hack or a liquidation, but it's a constant tax on trading that the disciplined manage and the careless ignore — to the steady detriment of their returns.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

What is slippage?

The difference between the price you expected and the price you actually got. You see BTC at $100,000, hit buy, fill at $100,050 — that $50 is slippage.

What causes slippage?

Price moving in the delay between your decision and execution, and large orders 'walking' through order book levels at progressively worse prices.

When is slippage worst?

High volatility, thin liquidity, large orders, and around high-impact news releases — especially when these combine. Stops can be gapped past entirely.

How do I minimize slippage?

Use limit orders (fill at your price or better), trade liquid pairs, keep orders reasonably sized, avoid news spikes, and set slippage tolerance where available.

Can my stop-loss slip?

Yes. A stop-market order becomes a market order when triggered, so in a fast crash it can fill well below your stop price. Size positions conservatively assuming stops might slip.

What to read next

- Understanding the Order Book & Market Depth

- Limit vs Market Orders

- Backtesting with OpenClaw: Tools & Limits

- Reading an Economic Calendar

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. market microstructure and execution literature; exchange order mechanics.