Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer. Security context: Three critical CVEs disclosed in OpenClaw in Q1 2026 (CVE-2026-25253, CVE-2026-32922) plus the ClawHavoc supply-chain attack (1,184 malicious skills). Always run v2026.4.12 or later. Full security assessment.

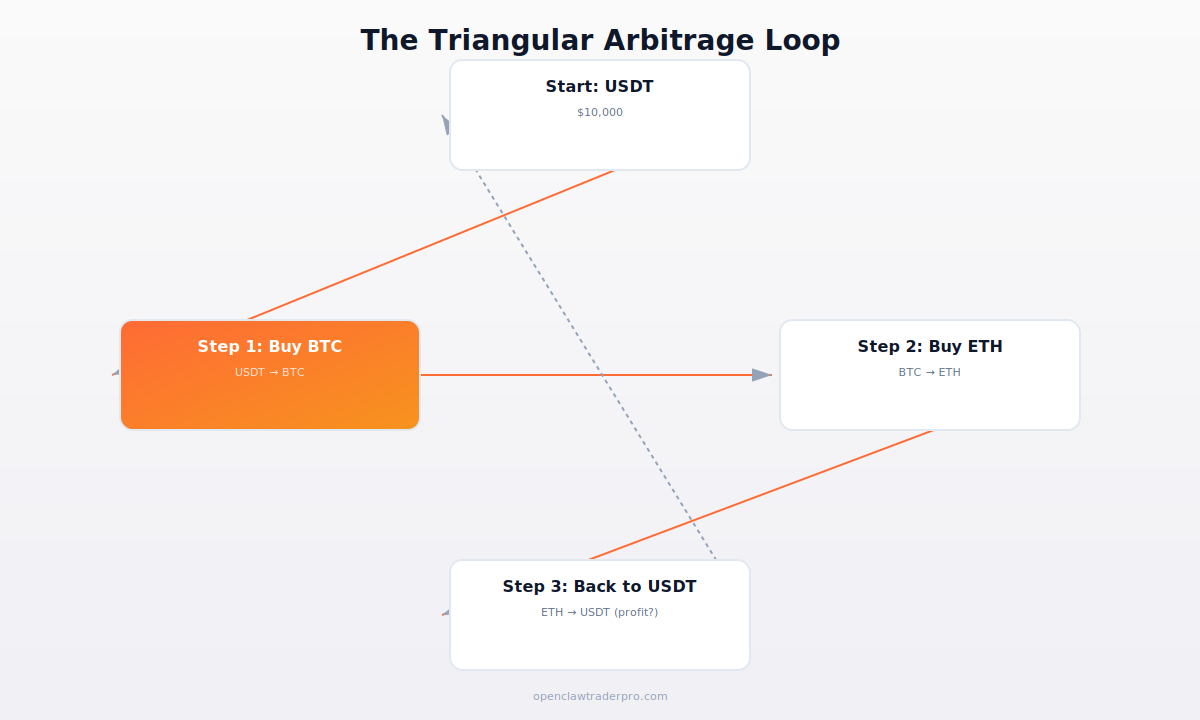

Triangular arbitrage looks like free money on paper: convert USDT to BTC, BTC to ETH, ETH back to USDT, and if the exchange rates are momentarily mispriced, you end up with more USDT than you started. Three trades, one cycle, risk-free profit. The theory is taught in every finance course. The reality for retail is that it's brutally hard to capture — the opportunities are tiny, fleeting, and contested by faster bots. This guide explains why.

We'll walk through the mechanics, the math, and the honest reasons most retail traders shouldn't expect to profit from triangular arbitrage — while acknowledging the narrow cases where it's possible.

TL;DR — The 30-second answer

- The idea: exploit price discrepancies across three trading pairs in a loop.

- The theory: risk-free profit if rates are momentarily mispriced.

- The reality: opportunities are tiny (often <0.1%), fleeting (milliseconds), and contested.

- The killers: fees, latency, slippage, and faster HFT bots.

- OpenClaw limitation: LLM latency (1.5-3s) is far too slow to capture these.

- Honest verdict: not a realistic retail strategy with OpenClaw. Educational, not practical.

The triangular loop

Here's the mechanic. You hold USDT. You execute three trades in a loop: buy BTC with USDT, buy ETH with that BTC, sell ETH back to USDT. If the three exchange rates are perfectly consistent, you end with exactly what you started (minus fees). But if they're momentarily inconsistent — say BTC/USDT, ETH/BTC, and ETH/USDT prices don't perfectly align — the loop can end with slightly more USDT than you began with. That discrepancy is the arbitrage profit.

This happens because prices on different pairs update at slightly different speeds. For a fraction of a second, the implied cross-rate (BTC→ETH via the two USDT pairs) might differ from the direct ETH/BTC rate. That window is the opportunity.

Why it's harder than it looks

Four brutal realities crush retail triangular arbitrage:

- The opportunities are tiny. Mispricings are usually well under 0.1%. After three sets of trading fees (typically 0.1% each, or 0.3% total round-trip), the discrepancy must exceed 0.3% just to break even. Discrepancies that large are rare and gone instantly.

- They're fleeting. Real arbitrage windows last milliseconds. By the time a human or a slow bot reacts, the prices have re-aligned. You need to detect and execute in microseconds.

- They're contested. Professional HFT firms run co-located servers specifically to capture these. They see the opportunity and execute before you've finished reading the order book. You're competing against teams with microsecond infrastructure.

- Slippage eats the rest. Even if you catch a window, executing three trades means three chances for slippage — the price moving between your order and the fill. On the tiny margins involved, slippage often turns a theoretical profit into a real loss.

Why OpenClaw specifically can't do this

This is a clear case where OpenClaw is the wrong tool. Triangular arbitrage requires sub-millisecond detection and execution. OpenClaw's LLM adds 1.5-3 seconds of latency per decision — that's roughly a million times too slow for an opportunity that lasts milliseconds. By the time OpenClaw's LLM has 'thought' about the trade, the window closed thousands of times over. For latency-critical strategies like this, you'd use a purpose-built low-latency engine (see Hummingbot vs OpenClaw), and even then, retail rarely competes with professional HFT.

The narrow cases where it's possible

Triangular arbitrage isn't entirely dead for non-HFT players, but the viable cases are narrow: on smaller, less efficient exchanges where HFT firms don't bother competing, larger and longer-lasting discrepancies occasionally appear. Some traders run dedicated low-latency bots (not OpenClaw) on these venues. But even there, the returns are thin, the competition is increasing, and the operational complexity (managing balances across pairs, handling failed legs) is significant. It's a specialist's game, not a retail OpenClaw strategy.

What to do instead

If you're drawn to arbitrage-style, market-neutral strategies (the appeal of 'risk-free' profit), funding rate arbitrage is far more realistic for retail — it's slower-moving, genuinely capturable, and suited to OpenClaw's pace. See our funding rate arbitrage guide. That's the market-neutral strategy worth your time; triangular arbitrage is best understood as educational — learn the concept, understand why it's contested, and move on to strategies you can actually execute.

The honest verdict

Triangular arbitrage is a beautiful concept and a terrible retail strategy with OpenClaw. The opportunities are too small, too fast, and too contested by infrastructure you can't match. Anyone selling a 'triangular arbitrage bot' that promises consistent profits is selling to people who haven't done this math. Understand it as theory, appreciate why markets are efficient, and direct your energy toward strategies that fit OpenClaw's strengths — reasoning, monitoring, and slower-moving edges like funding rate arbitrage.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

Is triangular arbitrage real?

The concept is real and occasionally occurs. But the opportunities are tiny (<0.1%), last milliseconds, and are dominated by HFT firms. It's not a realistic retail strategy.

Can OpenClaw do triangular arbitrage?

No. LLM latency (1.5-3s) is roughly a million times too slow for opportunities lasting milliseconds. Wrong tool entirely.

Why can't I profit from it?

Fees (0.3% round-trip) usually exceed the discrepancy; windows last milliseconds; HFT firms with co-located servers capture them first; slippage eats the rest.

Are 'triangular arbitrage bots' for sale legit?

Be very skeptical. The math makes consistent retail profit nearly impossible. These are usually sold to people who haven't done the math.

What market-neutral strategy works for retail?

Funding rate arbitrage — slower-moving, genuinely capturable, and suited to OpenClaw's pace. See our dedicated guide.

What to read next

- Funding Rate Arbitrage

- Hummingbot vs OpenClaw

- Crypto Arbitrage Realistic Expectations

- Scalping with Bots: Why LLM Latency Kills It

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. market microstructure literature; exchange fee schedules; HFT arbitrage research.