Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer.

Crypto arbitrage is the most-promised, least-delivered strategy in retail crypto trading. Every YouTube ad shows the same idea: "Bitcoin is $1 cheaper on Exchange A than Exchange B. Buy on A, sell on B, profit!" The pitch is correct in principle but wrong in practice. By the time you read this, the same opportunity has been arbitraged away — usually by bots operating in sub-100ms.

This guide lays out what crypto arbitrage actually looks like in 2026, what's still possible at LLM-inference speeds (which is what OpenClaw works with), and the realistic returns to expect.

TL;DR — The 30-second answer

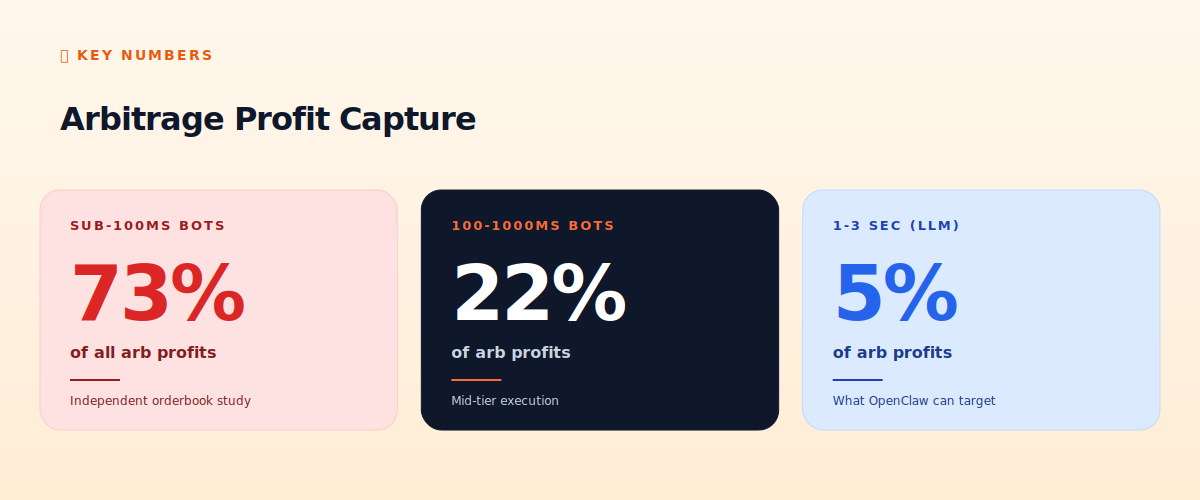

- 73% of arbitrage profits are captured by sub-100ms bots (sub-second VPSes, custom code).

- 22% by 100-1000ms bots (medium-tier execution).

- Only 5% remains for LLM-speed bots (1500-3000ms), which is what OpenClaw works with.

- Pure inter-exchange arbitrage is largely dead for retail.

- What still works: statistical arb (correlation-based), triangular arb on small exchanges, funding rate arb.

- Realistic returns: 1-5% per month, NOT the 30-50% YouTube claims.

The reality of crypto arbitrage profit capture

An independent study by a quantitative research group in early 2026 analyzed orderbook movements across the top 10 crypto exchanges over a 30-day period. The conclusion: when a price discrepancy appears between exchanges, it's typically arbitraged within 50-200 milliseconds. The bots that capture this are running on co-located VPSes with sub-100ms total latency including order placement.

By the time an LLM-driven bot (OpenClaw + Claude/GPT) processes a tick, decides to trade, and places an order — 1500-3000ms later — the discrepancy is gone. The exchange that was 0.3% cheaper is now back in line with the others.

This is why "arbitrage bot" tutorials on YouTube are systematically misleading. The strategy they describe was viable in 2017-2019. It hasn't been viable for retail since around 2022.

What still works for retail in 2026

1. Statistical arbitrage (correlation-based)

Instead of looking for instant price discrepancies, look for medium-term correlations between assets. Example: BTC and ETH typically move together with a correlation of 0.85+. When they diverge (BTC up 2%, ETH up 0.5%), you can long the laggard and short the leader, betting that the correlation will reassert.

Time horizon: hours to days. Required latency: seconds is fine. OpenClaw-friendly? Yes. Expected returns: 5-15% annual, low volatility.

2. Triangular arbitrage on smaller exchanges

Large exchanges (Binance, Bybit) are arbitraged second-by-second. Smaller exchanges — especially regional ones like Indodax (Indonesia), Bitkub (Thailand), CoinDCX (India) — have less arbitrage activity. Triangular arbitrage (BTC/USDT → ETH/BTC → ETH/USDT) sometimes shows 0.3-1% inefficiencies that survive for minutes.

Time horizon: minutes. Required latency: 1-2 seconds is acceptable. OpenClaw-friendly? Yes. Expected returns: 2-8% per month if you find live opportunities; can dry up suddenly when other bots discover the venue.

3. Funding rate arbitrage

When perpetual futures funding rates are very positive (longs paying shorts a lot), you can: long the spot, short the perpetual. You collect the funding rate while being neutral to BTC price. Risks: spot exchange goes down, perp exchange goes down, liquidation if you sized too aggressively.

Time horizon: hours to weeks. Required latency: none, this is structural. OpenClaw-friendly? Very. Expected returns: when conditions are right (high funding), 10-30% annualized on the spread; mostly idle otherwise.

4. Stablecoin yield arbitrage

Different lending platforms (Aave, Compound, Curve, exchange-native lending) offer different USDT/USDC yields. Move stablecoin across to capture the highest yield. Not arbitrage in the classic sense but similar mechanic.

Time horizon: days to weeks. Required latency: none. OpenClaw-friendly? Yes. Expected returns: 5-15% annualized on stablecoins, with low risk.

What doesn't work (despite the marketing)

- Cross-exchange spot arbitrage (the YouTube classic): systematic losses for retail.

- Cross-network arbitrage (BTC on Bitcoin vs WBTC on Ethereum): the bridge fees and confirmation times eat all profit.

- DEX vs CEX arbitrage: gas costs make small opportunities unprofitable; large opportunities are gone in < 1 block.

- NFT arbitrage: wash trading distorts signals. Real opportunities exist but require deep market knowledge.

- Memecoin arbitrage: illiquid, volatile, often subject to rug pulls. Don't.

Building a realistic OpenClaw arb bot

Recommendation: focus on funding rate arbitrage or statistical arbitrage. These work with LLM-speed decisions and don't require infrastructure you can't easily get.

Funding rate arbitrage skill outline:

# Every hour:

1. Query funding rates on Binance, Bybit, OKX for BTC, ETH, SOL perps.

2. If any > 0.05% per 8h:

a. Open spot long on Binance (cheapest spot).

b. Open perp short on exchange with high funding.

c. Size 1-2% of capital. Both legs equal notional.

3. Hold until funding drops below 0.02% or reverses.

4. Close both legs simultaneously.

5. Net result: funding payments collected, BTC price exposure zero.

Realistic monthly returns from funding arb when conditions are right: 2-5%. In quiet periods (Q1-Q2 2026 has been quiet), opportunities disappear for weeks. Don't expect constant action.

What the YouTube ads get wrong

- Profit per opportunity: they show $50 in 30 seconds. Real opportunities show $0.50 in 5 minutes after fees.

- Frequency of opportunities: they show "happens every minute." Real frequency is 2-10 per day for tradeable opportunities.

- Capital required: they show "start with $100." Real bot needs $5K+ to make meaningful returns after fees.

- Slippage: they show ideal limit-order fills. Reality is 0.1-0.5% slippage on market orders.

- Withdrawal time: they ignore the 30-60 minutes to move funds between exchanges. By then, opportunity is gone.

Honest expectations

If you do arbitrage well with OpenClaw and discipline: 1-5% per month, low volatility. Steady. Boring. The kind of returns that compound nicely but don't make YouTube videos.

If you do arbitrage poorly: 0% to -20% per month. Fees eat your equity. Failed trades pile up. Account drains slowly.

If you're promised 30%+ monthly from any arb strategy: that's not arbitrage. It's a different (riskier) strategy being mislabeled. Or it's a scam. Or it's survivorship bias of one lucky operator. None of these are repeatable.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

Can I really make money with arbitrage in 2026?

Yes, but realistically 1-5% per month with discipline. Not 30-50%. Funding rate arb and statistical arb are still viable.

Why are sub-100ms bots dominant?

Crypto markets are efficient at fast time scales. Bots running on co-located infrastructure see the same price faster than humans or LLMs can react.

Should I learn HFT to compete?

Probably not. The infrastructure cost (co-located VPS, custom code in Rust/C++, dedicated network lines) doesn't pay off until $1M+ in capital. Below that, slower strategies are more practical.

Is DeFi arbitrage better than CeFi?

Different. DEX vs CEX arb is theoretically possible but gas costs typically eat profits. DEX vs DEX same-chain works occasionally. Cross-chain is hard.

Can I just use a copy-trade or 'arb bot' service?

Almost all are scams or low-quality. The few legitimate services charge enough that you're paying their alpha. Better to learn and run your own.

What to read next

- OpenClaw + Binance Setup Guide

- Binance vs Bybit vs OKX

- CCXT Skill Deep Dive

- Hot Wallet Hygiene for Bots

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. Independent orderbook analysis study (Q1 2026); CCXT funding rate data; on-chain DEX analytics from Dune.