Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer. Security context: Three critical CVEs disclosed in OpenClaw in Q1 2026 (CVE-2026-25253, CVE-2026-32922) plus the ClawHavoc supply-chain attack (1,184 malicious skills). Always run v2026.4.12 or later. Full security assessment.

Funding rate arbitrage is one of the few genuinely repeatable market-neutral strategies accessible to retail, and it's well-suited to OpenClaw's pace. The idea: hold a spot position and an offsetting perpetual futures position, collecting the funding rate payments while remaining hedged against price movement. When done right, it produces a yield largely independent of whether the market goes up or down. This guide explains the mechanics, the realistic yields, and the very real risks.

Unlike triangular arbitrage (too fast) or market making (too competitive), funding rate arbitrage moves slowly enough that OpenClaw can genuinely execute and manage it. That makes it worth understanding properly.

TL;DR — The 30-second answer

- The idea: hold spot + offsetting perpetual short; collect funding while hedged.

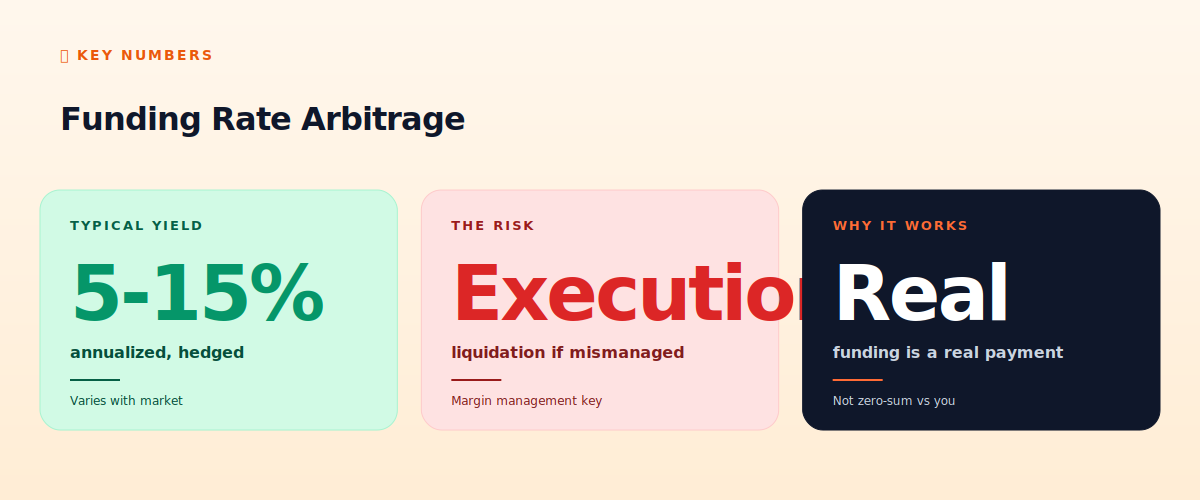

- Why it works: funding is a real payment between longs and shorts, not zero-sum vs you.

- Realistic yield: 5-15% annualized, hedged, varying with market conditions.

- The main risk: execution and liquidation if margin is mismanaged.

- OpenClaw fit: good — slow enough for the LLM to manage properly.

- Not risk-free: 'delta-neutral' reduces price risk, not all risk.

How it works

Perpetual futures use a 'funding rate' to keep their price tethered to the spot price. When the perpetual trades above spot (more longs than shorts), longs pay shorts a periodic funding payment (typically every 8 hours). When it trades below spot, shorts pay longs. This funding rate is the mechanism that anchors perpetuals to reality — and it's the source of the arbitrage.

The strategy: when funding is positive (longs paying shorts), you buy spot (e.g., 1 BTC on the spot market) and simultaneously short the equivalent perpetual (short 1 BTC perpetual). Your net exposure to BTC's price is zero — if BTC rises, your spot gains and your short loses equally; if BTC falls, vice versa. You're delta-neutral. But because you're short the perpetual while funding is positive, you collect the funding payment every 8 hours. That collected funding, minus fees, is your profit — earned regardless of price direction.

Why this is a genuine edge

Unlike binary options or grid trading, funding rate arbitrage isn't a bet against the house or a directional gamble. The funding payment is a real transfer built into the perpetual futures mechanism — longs genuinely pay shorts. By positioning as the hedged short during positive funding, you collect a real cash flow. It's not zero-sum against you the way a broker-counterparty product is. This is why it's one of the few strategies we'd call a genuine, repeatable retail edge.

Realistic yields

Funding rates vary with market sentiment. In strong bull markets with heavy long demand, funding can be very high (annualized 20-50%+ briefly). In calm or bearish markets, it can be near zero or negative. Averaged over time, a well-managed funding rate arbitrage operation realistically yields 5-15% annualized, hedged. That's a solid, market-neutral return — better than most 'safe' yields — but it's not the 'risk-free 50%' some promote. The yield comes with real risks, covered next.

The real risks

'Delta-neutral' means hedged against price direction — it does not mean risk-free. The risks:

- Liquidation risk. Your short perpetual position uses margin. If BTC pumps hard and you haven't allocated enough margin, the short can be liquidated — at which point you're no longer hedged and exposed to the full move. Proper margin management is critical.

- Funding flips negative. If funding turns negative (shorts paying longs), your collected cash flow reverses into a cost. You need to monitor and exit or flip when conditions change.

- Execution risk. Opening and closing two positions (spot + perpetual) means execution complexity and slippage on both legs. Mismatched fills leave you imperfectly hedged.

- Exchange/counterparty risk. Your capital sits on an exchange. The usual crypto exchange risks apply (see our wallet hygiene guide).

Where OpenClaw fits

Funding rate arbitrage moves on an 8-hour funding cycle — slow enough that OpenClaw's LLM latency is irrelevant. This makes it a genuine fit. An OpenClaw funding-arb skill can: monitor funding rates across exchanges, identify when positive funding justifies opening a hedged position, open the spot+short pair with proper margin allocation, monitor margin health every heartbeat, collect funding, and exit or rebalance when funding flips or margin gets tight. The LLM's judgment helps with the 'when conditions change' decisions that a dumb bot handles poorly.

Critical guardrails: never over-allocate margin to the short (liquidation is the main killer), monitor margin ratio on every heartbeat with alerts, and hard-cap position size. We detail the guardrail philosophy in the hardening checklist.

The honest verdict

Funding rate arbitrage is one of the few strategies in this entire site we'd call a genuine, repeatable retail edge — because the funding payment is real, the strategy is market-neutral, and the pace suits OpenClaw. But 'genuine edge' doesn't mean 'easy' or 'risk-free.' Liquidation risk from poor margin management is the most common way operators turn a hedged position into a loss. Done with discipline — conservative margin, constant monitoring, realistic yield expectations — it's a sound strategy. Done carelessly, the liquidation on your short erases months of collected funding in one bad pump.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

Is funding rate arbitrage risk-free?

No. 'Delta-neutral' means hedged against price direction, not risk-free. Liquidation risk (if margin is mismanaged), funding flips, and execution risk are all real.

What yield is realistic?

5-15% annualized, hedged, averaged over time. Funding rates spike in bull markets and fade in calm ones. Not the 'risk-free 50%' some promote.

Why does this strategy work?

Funding is a real payment between longs and shorts, built into perpetual futures. Positioning as the hedged short during positive funding collects real cash flow — not zero-sum against you.

Can OpenClaw run this?

Yes — the 8-hour funding cycle is slow enough that LLM latency doesn't matter. It's a genuine OpenClaw fit, unlike fast arbitrage.

What's the biggest risk?

Liquidation of your short leg from insufficient margin during a price pump. Conservative margin allocation and constant monitoring are essential.

What to read next

- Triangular Arbitrage: Why It's Hard

- Spot vs Futures for Beginners

- OpenClaw + Bybit Futures Tutorial

- Crypto Arbitrage Realistic Expectations

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. perpetual futures funding mechanics from exchange documentation; delta-neutral strategy literature.