Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer.

Risk of ruin is the probability that you lose so much of your capital that you can't continue trading — that you're wiped out. It's the most important concept in trading and the most ignored, because it's about survival rather than profit, and survival is unglamorous. This guide explains the math intuitively, shows why position sizing is the master variable, and makes the case that staying in the game is the prerequisite for every other strategy working. It's the capstone of the beginner series for a reason.

Every other guide teaches you how to trade. This one teaches you how to not get knocked out before your edge has time to work. If leverage is what kills beginners fast, ignoring risk of ruin is what kills them slowly.

TL;DR — The 30-second answer

- Risk of ruin is the probability of losing enough capital that you can't continue.

- The key variable is how much you risk per trade — position sizing.

- Risking too much per trade makes ruin likely even with a winning strategy.

- Risking ~1% per trade makes drawdowns survivable, letting your edge play out.

- Survival first, profit second: you can't profit if you're knocked out.

- The math is unforgiving — recovering from big losses is harder than avoiding them.

The risk of ruin

What risk of ruin means

Risk of ruin is the probability that a series of losses depletes your capital to the point where you can't keep trading — either literally zero, or low enough that recovery is practically impossible. It depends on three things: your edge (win rate and risk:reward — do you make money on average?), your position sizing (how much you risk per trade), and the number of trades you take. Of these, position sizing is the one you most directly control, and it's the dominant factor in whether you survive.

The brutal math of recovery

Before the ruin math, understand why big losses are so dangerous: losses and gains are asymmetric. If you lose 50% of your account, you need a 100% gain just to get back to even — not 50%. The deeper the hole, the disproportionately harder the climb out:

- Lose 10% → need +11% to recover. Manageable.

- Lose 25% → need +33% to recover. Harder.

- Lose 50% → need +100% to recover. Very hard.

- Lose 75% → need +300% to recover. Nearly impossible.

- Lose 90% → need +900% to recover. Effectively done.

This asymmetry is why avoiding large losses matters more than capturing large gains. A trader who never lets a loss get catastrophic stays in a position to compound; one who takes a 75% drawdown faces a recovery so steep that they're effectively ruined even if not literally at zero.

Why position sizing is the master variable

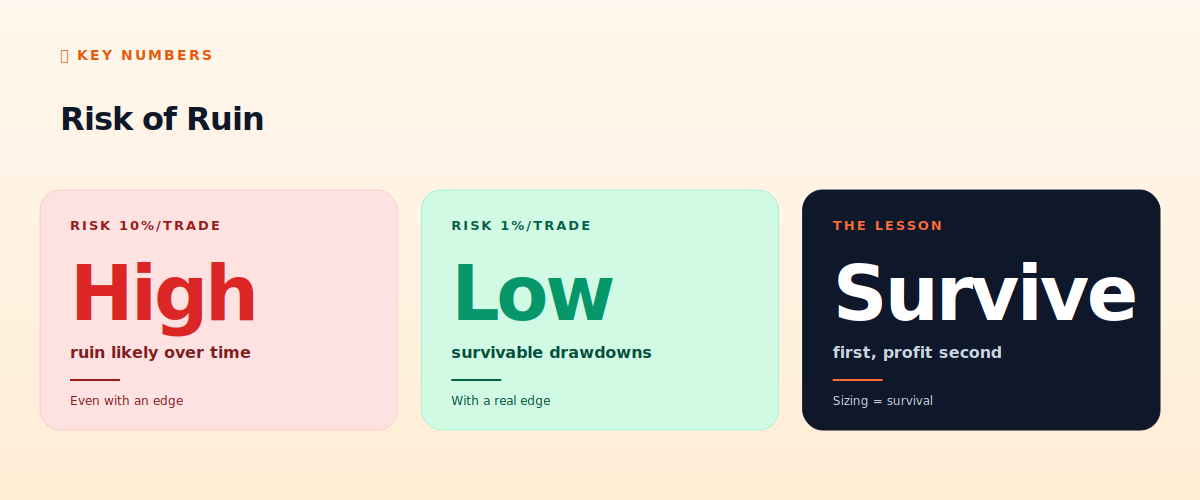

Here's the core insight: even a profitable strategy can ruin you if you bet too big per trade. Suppose you have a genuine edge — you win 55% of trades at 1:1 risk:reward, a solid edge. If you risk 50% of your account per trade, two consecutive losses (which will happen regularly) take you down 75% — near-ruin — despite your edge. The edge is real, but you didn't survive long enough to realize it. Conversely, risk 1% per trade with that same edge, and even a string of 10 losses (rare but possible) only draws you down ~10% — survivable, and your edge compounds over time.

This is the counterintuitive truth: how much you risk per trade matters more than how good your strategy is. A mediocre strategy with tiny position sizes survives; a great strategy with reckless sizing gets wiped out by a normal losing streak. Position sizing isn't a detail — it's the difference between survival and ruin.

The 1% rule

The widely-cited guideline: risk no more than 1% (some say up to 2%) of your account on any single trade. 'Risk' here means the amount you'd lose if your stop-loss is hit — not your position size, but your loss if wrong. With a $10,000 account, risking 1% means structuring each trade so a stop-out loses $100. This connects directly to our stop-loss guide and lot sizing guide: you set your stop based on the trade, then size your position so the distance to the stop equals 1% of your account.

Why 1%? Because it makes losing streaks survivable. Even 10 consecutive losses (which happens) only costs ~10% — a drawdown you recover from. It keeps you in the game long enough for your edge (if you have one) to play out over many trades. The math of risk of ruin shows that at 1% risk per trade with even a modest edge, the probability of ruin becomes very small. At 10% per trade, ruin becomes likely regardless of edge.

The connection to martingale

This is the mathematical foundation of why martingale (doubling after losses) is so deadly: it does the exact opposite of sound position sizing, dramatically increasing risk after losses precisely when you should preserve capital. Martingale maximizes risk of ruin while disguising it with frequent small wins. Understanding risk of ruin makes martingale's fatal flaw obvious: it's an engine for guaranteeing the ruinous streak. Sound position sizing (constant small risk) and martingale (escalating risk) are mathematical opposites — one is built for survival, the other for eventual destruction.

Survival first, profit second

The mindset shift this concept demands: your first job as a trader is not to make money — it's to not get knocked out. Profit is impossible if you're ruined. Every professional trader and risk manager prioritizes survival: conservative position sizing, hard stops, never risking ruin on any single trade or even a bad streak. This sounds unexciting compared to 'how to find winning trades,' but it's the foundation everything else rests on. The trader who survives a hundred trades with disciplined sizing has a hundred chances for their edge to work; the one who blows up on trade five has zero. Boring survival beats exciting ruin.

For bot traders

In OpenClaw bots, risk of ruin discipline is enforced through hard-coded guardrails (from our hardening checklist): a strict per-trade risk cap (e.g. 1%), a daily-loss kill-switch that halts trading after a defined drawdown, and position-size limits that no signal can override. The bot's advantage is that it enforces these mechanically — it never gets greedy and oversizes, never moves a stop, never revenge-trades after a loss. Building risk-of-ruin discipline into the bot's structure is arguably more important than the strategy logic itself, because it's what keeps the account alive long enough for the strategy to matter.

The honest verdict

Risk of ruin is the most important concept in trading because it governs survival, and survival precedes profit. The math is unforgiving: large losses are disproportionately hard to recover from, and reckless position sizing can ruin you even with a genuine edge. The defense is simple to state and hard to follow: risk a small, constant fraction (~1%) of your account per trade, use stops, and never let a single trade or streak threaten your ability to continue. Get this right and you give your edge time to work; get it wrong and no amount of clever strategy saves you. If you take one lesson from this entire beginner series, let it be this: protect your capital first, and the profits become possible.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

What is risk of ruin?

The probability of losing enough capital that you can't continue trading. It depends on your edge, position sizing, and number of trades — with position sizing the variable you most control.

Why is position sizing so important?

Even a profitable strategy can ruin you if you bet too big. Risk 50% per trade and two losses nearly wipe you out despite an edge. Risk 1% and you survive losing streaks. Sizing matters more than strategy quality.

What is the 1% rule?

Risk no more than 1% of your account on any single trade — meaning your loss if the stop is hit. It makes losing streaks survivable (10 losses = ~10% drawdown) so your edge can play out.

Why are big losses so dangerous?

Recovery is asymmetric. Lose 50% and you need +100% to recover; lose 75% and you need +300%. The deeper the hole, the disproportionately harder the climb — so avoiding big losses beats chasing big gains.

How does this relate to martingale?

Martingale does the opposite of sound sizing — increasing risk after losses, maximizing risk of ruin while hiding it behind small wins. Understanding risk of ruin makes martingale's fatal flaw obvious.

What to read next

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. risk of ruin probability theory; position sizing and money management literature.