Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer.

The single most important skill in retail forex trading is position sizing — specifically, the discipline to size every trade so that a typical adverse move costs no more than 1% of your account. This is boring math, and it's the difference between the 70% who blow up and the 30% who survive.

This guide covers the actual lot-sizing math, the pip-value formulas you need, the stop-placement principles that follow from the math, and how to encode all of this into a hard-guard SKILL.md that OpenClaw can't violate. None of this is novel — it's been the standard advice for 30 years. The novelty is encoding it into code so the LLM never "forgets."

TL;DR — The 30-second answer

- The 1% rule: never risk more than 1% of account equity on a single trade.

- Lot size formula: lot_size = (risk_amount) / (stop_loss_pips × pip_value).

- Pip value for EUR/USD: $10 per pip on 1 lot ($100K nominal); $1 per pip on 0.1 lots.

- For volatile pairs (GBP/JPY): use smaller size due to wider stops needed.

- Daily loss limit: 3-5% hard cap. Hit it = stop trading for the day.

- Maximum simultaneous risk: 5-6% across all open positions.

The 1% rule explained

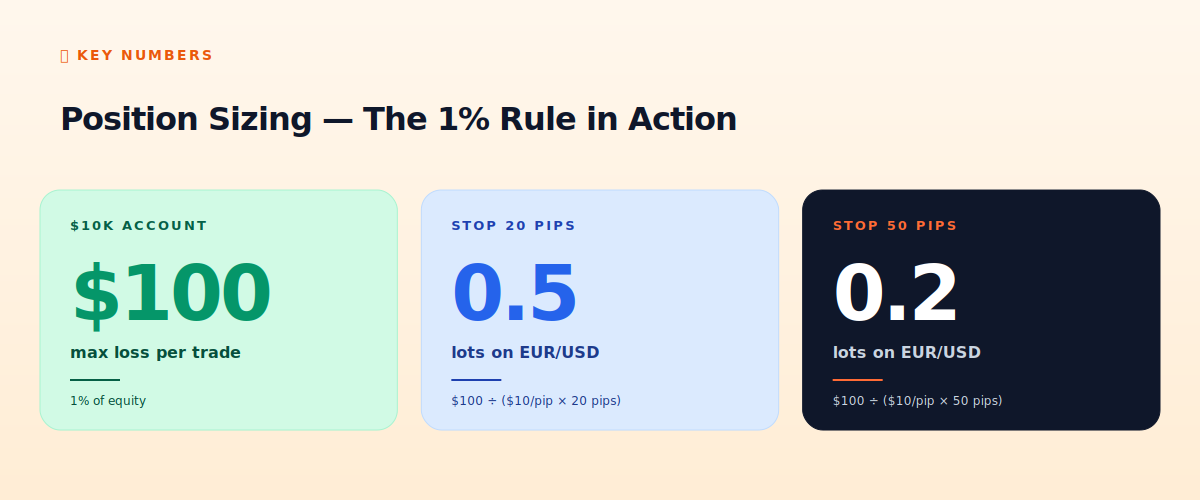

On a $10,000 account, the 1% rule means no single trade should risk more than $100. "Risk" here is the distance from entry to stop loss, multiplied by position size. If your stop is 20 pips away on EUR/USD and each pip costs you $10 on 1 lot, then 0.5 lots is the right size: 20 pips × $10/pip × 0.5 lot = $100 risk.

Why 1% and not 2% or 5%? Kelly criterion math. If you have a 55% win rate with 1:1 risk-reward (typical for solid forex strategies), Kelly says optimal sizing is ~10% per trade — but with high variance, you'll have 10-trade losing streaks that wipe accounts at that size. The standard adjustment is fractional Kelly, typically 1/10 of full Kelly = 1% per trade. Boring, but it survives drawdowns.

The lot sizing formula

lot_size = risk_amount / (stop_loss_pips × pip_value_per_lot)

Pip value per 1 standard lot on major pairs:

- EUR/USD, GBP/USD, AUD/USD, NZD/USD: $10 per pip per 1 lot

- USD/JPY: ~$10 per pip per 1 lot (varies slightly with current price)

- USD/CHF, USD/CAD: ~$10 per pip per 1 lot

- GBP/JPY, EUR/JPY (cross-yen): ~$10 per pip per 1 lot

- GBP/NZD, EUR/AUD (exotic crosses): $10-15 per pip per 1 lot

Standard lot = 100,000 units. Mini lot = 10,000 units = 0.1 standard lot. Micro lot = 1,000 units = 0.01 standard lot. Most retail forex brokers allow trading down to 0.01 lots, which is $0.10 per pip on EUR/USD — small enough that almost any account can practice.

Stop loss placement principles

Lot sizing follows stop placement, not the other way around. You don't pick a lot size first and then figure out where to put the stop — that's how accounts die. The correct order is:

- Identify entry point.

- Identify logical stop loss location (above recent swing high for short, below swing low for long, or based on volatility like 1.5x ATR).

- Measure distance from entry to stop in pips.

- Compute lot size to make that stop = 1% of account.

- Place trade with size and stop.

If the resulting lot size is smaller than your broker's minimum (typically 0.01), the trade isn't viable for your account size — skip it. If the lot size is unusually large because the stop is very tight, double-check the stop location; tight stops on volatile pairs get hit by noise.

Daily loss limit — the kill-switch

Beyond per-trade sizing, you need a daily loss limit. Standard: 3-5% of starting equity per day. Once you hit that, stop trading for the day. No exceptions.

Why this matters: emotional revenge trading is the #1 cause of account blowup. After 3-5 losing trades in a row, almost every human (and many LLMs) try to "win it back" by increasing size or trading without proper setups. The daily limit hard-stops this pattern.

Implementation in SKILL.md:

# Before any order:

start_equity = get_start_of_day_equity() # cached at 00:00 UTC daily

current_equity = mt5.account_info().equity

daily_pnl_pct = (current_equity - start_equity) / start_equity

if daily_pnl_pct < -0.05:

refuse_order()

telegram_alert("Daily loss limit hit. Trading halted.")

return

Concurrent risk management

If you trade multiple pairs simultaneously, the total open risk across all positions must be capped. Standard: 5-6% maximum across all open positions.

This matters because correlations matter. If you're long EUR/USD and long GBP/USD (both correlated ~0.85), the two positions move together. A bad EUR/USD news event probably also hurts GBP/USD. Treating them as independent 1% risks gives you 2% concentrated risk on the same underlying.

Practical rule: if you're already in 1 EUR/USD position, don't open a 2nd correlated position (GBP/USD, AUD/USD long, NZD/USD long). If you must, size the second position 0.5% instead of 1% to reflect the correlation.

Risk-reward ratio

Position sizing handles "how much can I lose." Risk-reward ratio handles "how much can I win for what I risk." Standard advice is to require at least 1:2 risk-reward — risking 20 pips to make 40+. The math: at 1:2 R:R, you can have a 40% win rate and still be profitable. At 1:1, you need above 55%. At 1:0.5 (risking more than you make), you need 70%+ — nearly impossible to sustain.

In your SKILL.md, encode this as: every trade must have take_profit set to at least 2x the stop_loss distance. Trades without TP set should be flagged as exceptions requiring user confirmation.

What to do during drawdowns

When your account is down 10%+ from peak, do NOT increase position size to "recover faster." The correct response is the opposite: reduce size by 50% until you've recovered to within 5% of peak.

This is the opposite of what your gut tells you. It's also what survives. The math is simple: if you're losing at 1% sizes, you'll lose faster at 2% sizes. The strategy isn't working right now; smaller positions buy you more time to figure out why before you blow up.

Implementation: store your account peak balance. If current balance < 0.9 × peak, multiply position size by 0.5 in the SKILL.md. When recovered to within 5%, revert to normal sizing.

Complete hard-guard SKILL.md template

---

name: forex-position-sizer

description: "Compute and enforce forex position sizing."

permissions:

- network

---

Given a trade request with: symbol, direction, entry, stop_loss_pips, take_profit_pips:

1. Verify symbol in approved list.

2. Get current account equity and peak equity.

3. If equity < 0.9 × peak: size_multiplier = 0.5. Else: 1.0.

4. risk_amount = equity × 0.01 × size_multiplier.

5. pip_value = lookup_pip_value(symbol).

6. lot_size = round(risk_amount / (stop_loss_pips × pip_value), 2).

7. If lot_size < 0.01: REFUSE (trade too small).

8. If take_profit_pips < 2 × stop_loss_pips: REQUIRE user confirmation.

9. Check daily P&L. If < -0.05: REFUSE.

10. Check concurrent risk: total open position risk must stay < 0.06.

11. Place order via mt5.create_order().

12. Telegram alert on placement.

13. Log to ~/.openclaw/logs/sizing.jsonl.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

Can I size larger than 1% if I'm confident?

Confidence is the worst predictor of strategy edge. Stick to 1% even when you're sure. Especially when you're sure — that's when overconfidence kicks in.

What if I want to use Martingale?

Don't. Martingale (doubling after losses) mathematically guarantees eventual ruin. It's the strategy YouTube ads promote and it's the strategy that eats accounts.

Should the LLM compute lot size?

The LLM can compute it, but a hard-coded function should also enforce it. Belt and suspenders — LLMs occasionally hallucinate math.

What about scaling into positions?

Add to winners, never to losers. The 1% risk should be applied to the total maximum size you'd build, not the initial entry. Plan the full scale-in before opening the first position.

Can I have a larger daily limit on news days?

Lower it, not higher. News increases unpredictability; the right response is more conservative sizing, not less.

What to read next

- Forex Trading with OpenClaw

- OpenClaw + MT5 Setup

- 4 Forex Strategies That Actually Work

- The 12-Point Hardening Checklist

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. Edward Thorp Kelly criterion papers; ESMA position-sizing guidelines for retail; standard CFA risk-management curriculum.