Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer. Security context: Three critical CVEs disclosed in OpenClaw in Q1 2026 (CVE-2026-25253, CVE-2026-32922) plus the ClawHavoc supply-chain attack (1,184 malicious skills). Always run v2026.4.12 or later. Full security assessment.

After exploring individual strategies, the natural next step is combining them. A single strategy — however good — has periods where it struggles: grid bleeds in trends, momentum whipsaws in ranges, funding arbitrage yields little in calm markets. By running multiple uncorrelated strategies together, the strong performers can offset the strugglers, smoothing overall returns. This guide covers how serious operators build a multi-strategy OpenClaw portfolio, the principle of diversification, and the risk management that ties it together.

This is the capstone of the strategy series: not a new strategy, but the architecture for combining them intelligently. It's how you move from running one bot to running a coordinated operation.

TL;DR — The 30-second answer

- The idea: run multiple uncorrelated strategies; winners offset strugglers.

- The principle: diversification — strategies that win in different regimes.

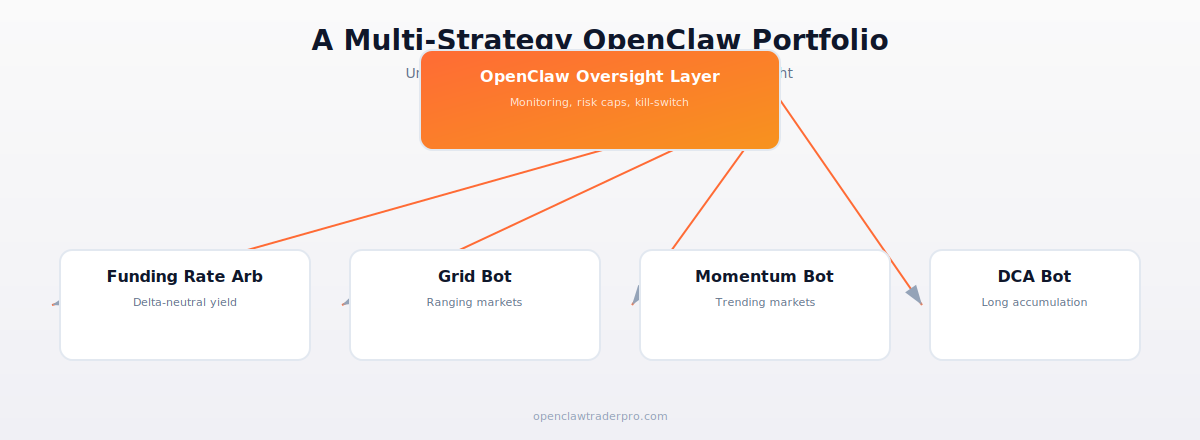

- Example mix: funding arb + grid + momentum + DCA, each for its regime.

- The architecture: isolated strategies, unified OpenClaw oversight layer.

- Risk management: portfolio-level caps on top of per-strategy guardrails.

- The goal: smoother returns and lower drawdowns than any single strategy.

The portfolio architecture

Why diversify strategies

Every strategy in this series has a regime where it thrives and a regime where it struggles. Grid trading earns in ranging markets and bleeds in trends. Momentum wins in trends and whipsaws in ranges. Funding rate arbitrage yields well when funding is high and little when it's flat. Mean reversion profits in ranges and gets cut by trends. No single strategy works in all conditions — which means a single-strategy operator has good periods and painful periods dictated entirely by whether the current market suits their one approach.

The insight: if you run several strategies that thrive in different regimes, then whatever the market is doing, something in your portfolio is working. When the market trends, your momentum bot earns while your grid sits paused; when it ranges, the grid earns while momentum stands aside; funding arbitrage chugs along in the background regardless. The strong performers offset the strugglers, and your overall return is smoother than any single strategy's. This is diversification applied to strategies rather than assets.

An example portfolio

A balanced multi-strategy OpenClaw portfolio might combine:

- Funding rate arbitrage (see our guide): a market-neutral base layer providing steady hedged yield largely independent of market direction.

- A grid bot on a ranging pair: capturing oscillations, paused by regime detection when a trend emerges.

- A momentum bot: catching sustained trends when they appear, standing aside in chop.

- A DCA bot (see our guide): slowly accumulating a long-term-conviction asset in the background.

These are genuinely uncorrelated: funding arb doesn't care about direction, grid wants ranges, momentum wants trends, DCA accumulates regardless. In any given market condition, the portfolio has at least one strategy in its favorable regime. The key word is uncorrelated — running four momentum bots isn't diversification, it's concentration. The strategies must win in different conditions for diversification to work.

The OpenClaw oversight layer

This is where OpenClaw's architecture shines. Rather than four disconnected bots, you build a unified system: each strategy runs in isolation (separate logic, separate position tracking, ideally separate sub-accounts), but a single OpenClaw oversight layer monitors them all. The oversight layer:

- Monitors each strategy's performance, positions, and health.

- Enforces portfolio-level risk caps on top of each strategy's own guardrails (more on this below).

- Detects regime and can activate/pause strategies as conditions change (pause the grid when a trend starts, etc.).

- Alerts you to anything unusual across the whole portfolio via Telegram (see our Telegram guide).

- Provides a kill-switch that can flatten everything across all strategies at once.

This unified oversight is the difference between a coordinated operation and four bots that might collectively over-expose you without any of them individually noticing.

Portfolio-level risk management

The critical addition in a multi-strategy setup is portfolio-level risk caps layered on top of per-strategy guardrails. The danger: each strategy might respect its own 1% position limit, but if all four simultaneously take correlated risk (e.g. all long crypto during a crash), the portfolio's aggregate exposure could be dangerous even though no single strategy violated its rules. The oversight layer must enforce:

- Aggregate exposure cap: total position across all strategies can't exceed a portfolio limit, regardless of individual strategy limits.

- Portfolio daily-loss kill-switch: if the whole portfolio is down X% on the day, halt everything — not just the strategy that triggered it.

- Correlation monitoring: watch for strategies inadvertently taking the same directional bet, concentrating risk.

- Capital allocation limits: each strategy gets a fixed slice of capital; none can grow to dominate the portfolio.

These build on the per-strategy guardrails from our hardening checklist — portfolio-level caps are an additional layer, not a replacement.

Start simple, add gradually

Don't build a four-strategy portfolio on day one. The right path: master one strategy first (paper, then small live, then proven), add a second uncorrelated one once the first is stable, build the oversight layer as you go, and only expand to three or four once you can manage the complexity. A multi-strategy portfolio is more capable but also more complex — more to monitor, more failure modes, more that can go wrong silently. Add complexity only as fast as you can manage it. A well-run single strategy beats a poorly-managed portfolio.

The honest verdict

A multi-strategy portfolio is how serious operators reduce the regime-dependence that limits any single strategy, smoothing returns and lowering drawdowns through genuine diversification. OpenClaw's architecture — isolated strategies under a unified reasoning-driven oversight layer — suits this well. But it's an advanced setup: it requires that you've mastered the individual strategies, can build robust portfolio-level risk management, and can handle the added operational complexity. Build toward it gradually. Done right, it's the most robust way to run automated trading; done prematurely, it's just more ways to lose money at once. As with everything in this series: realistic expectations, rigorous risk management, paper-test, start small, and never deploy capital you can't afford to lose.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

What is a multi-strategy portfolio?

Running several uncorrelated strategies together so that strong performers offset strugglers, smoothing overall returns. Diversification applied to strategies, not just assets.

Why combine strategies?

Every strategy has regimes where it thrives and struggles. Uncorrelated strategies that win in different conditions mean something is always working, whatever the market does.

What's an example mix?

Funding rate arbitrage (market-neutral base) + grid (ranges) + momentum (trends) + DCA (long accumulation). Genuinely uncorrelated — they win in different conditions.

What's the key risk in a portfolio?

Aggregate exposure. Each strategy might respect its own limits, but if all take correlated risk simultaneously, the portfolio over-exposes you. Portfolio-level caps are essential.

Should beginners build a multi-strategy portfolio?

No. Master one strategy first, add a second once it's stable, expand gradually. A well-run single strategy beats a poorly-managed portfolio.

What to read next

- Funding Rate Arbitrage

- Grid Trading with OpenClaw

- DCA Bots: Automating Dollar-Cost Averaging

- The 12-Point Hardening Checklist

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. portfolio theory and diversification literature; OpenClaw orchestration patterns.