Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer.

Dollar-cost averaging (DCA) and lump-sum investing are two ways to deploy capital, and the debate between them is one of the most studied questions in finance. The data has a clear answer that conflicts with what most people's psychology prefers — which is exactly why the debate persists. This comparison covers what the research actually shows and why the 'right' choice depends on more than just math.

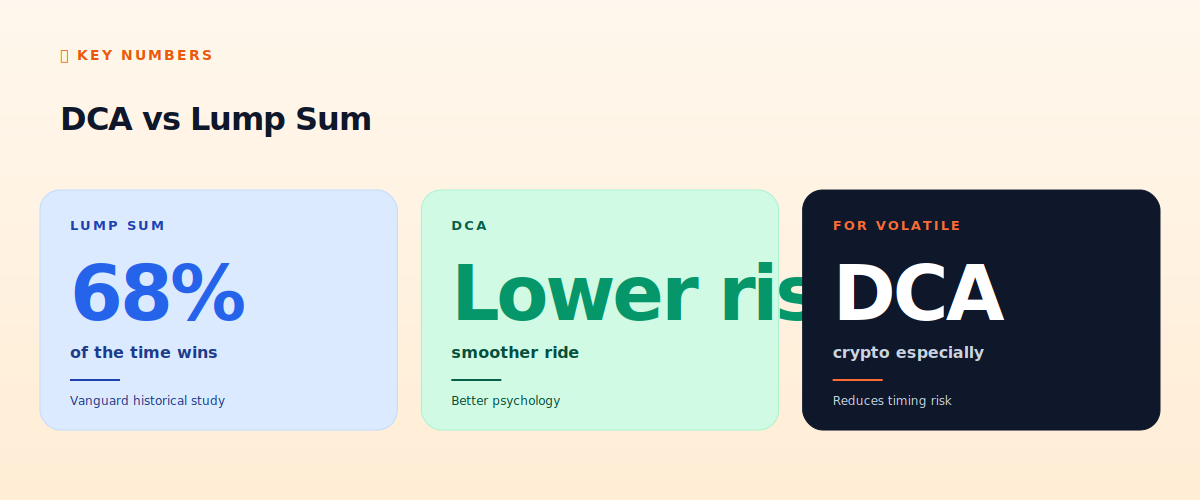

We compare DCA and lump-sum on expected returns, risk, psychology, and the specific case of volatile assets like crypto.

TL;DR — The 30-second answer

- Lump sum wins about 68% of the time historically (Vanguard study).

- DCA reduces risk and regret — smoother ride, better psychology.

- The math favors lump sum; the psychology favors DCA.

- For volatile assets (crypto): DCA's risk reduction is more valuable.

- For most people: DCA's behavioral benefits outweigh the small return cost.

- The best plan is the one you'll actually stick to.

What the data says

The lump-sum advantage

Vanguard's well-known historical study found that lump-sum investing outperformed dollar-cost averaging roughly 68% of the time across US, UK, and Australian markets over the periods studied. The logic is simple: markets rise more often than they fall, so deploying capital sooner means more time in the market capturing those gains. On average, sooner beats later.

This is the math case: if you have a lump sum and you believe the asset will rise over your horizon, deploying it all at once maximizes expected return. Statistically, waiting to DCA in costs you the average upward drift during the wait.

The DCA advantage

DCA — investing fixed amounts at regular intervals — wins on risk reduction and psychology, even though it loses on average return. Its benefits:

- Reduces timing risk. You don't deploy everything at a single (possibly bad) moment. If the market drops right after you'd have lump-summed, DCA saves you from that.

- Smoother ride. Your average entry price is less extreme. Smaller drawdowns from your entry point.

- Better psychology. DCA removes the agony of 'is now the right time?' and the regret of buying right before a crash. You just invest on schedule.

- Buys more when prices are low. Fixed-dollar amounts buy more units when prices dip, fewer when they rise — a mild automatic discipline.

The psychology that breaks the math

Here's why DCA persists despite the math favoring lump sum: most people can't emotionally handle lump-summing right before a drop. If you deploy your entire savings and the market falls 20% the next month, the regret and panic often cause you to sell at the bottom — turning a paper loss into a realized one. DCA's smoother ride keeps you invested through volatility because the emotional swings are smaller.

The best investment plan isn't the one with the highest expected return on a spreadsheet — it's the one you'll actually stick to through fear and greed. For most people, that's DCA, even at the cost of some expected return. A plan you abandon at the worst moment is worse than a slightly suboptimal plan you follow consistently.

The crypto case

For volatile assets like crypto, DCA's case strengthens. Crypto's extreme volatility (50%+ drawdowns are routine) makes lump-sum timing risk severe — lump-summing into BTC right before a 60% drawdown is psychologically devastating and historically common. DCA into crypto smooths this dramatically. The higher the volatility, the more DCA's risk reduction matters relative to its return cost. For crypto specifically, we lean DCA for most people.

How this relates to bot trading

This comparison is about investing (deploying capital into assets you hold), not active trading (the bot strategies most of this site covers). But the principle transfers: emotional sustainability matters as much as expected return. A trading approach you'll abandon under stress is worse than a slightly less optimal one you'll maintain. Whether you're DCAing into BTC or running an OpenClaw bot, the plan you can stick to beats the theoretically optimal plan you can't.

The verdict

The math favors lump sum (~68% of the time). The psychology favors DCA (smoother ride, less regret, easier to stick with). For a disciplined investor with a long horizon and strong stomach, lump sum maximizes expected return. For most people — and especially for volatile assets like crypto — DCA's behavioral benefits outweigh the small return cost. Choose the approach you'll actually maintain through a downturn; that consistency matters more than the marginal return difference.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

Which makes more money, DCA or lump sum?

Lump sum, about 68% of the time historically (Vanguard). Markets rise more than they fall, so deploying sooner captures more upside on average.

Why do people recommend DCA then?

Risk reduction and psychology. DCA's smoother ride keeps people invested through volatility, avoiding the panic-selling that destroys lump-sum returns in practice.

Which is better for crypto?

DCA, for most people. Crypto's extreme volatility makes lump-sum timing risk severe; DCA smooths it significantly.

Is DCA always safer?

Lower variance of outcomes, yes. But it's not 'safe' — you can still lose money if the asset declines over your whole DCA period.

How does this apply to trading bots?

It's about investing, not active trading. But the principle transfers: a sustainable plan you'll stick to beats an optimal one you'll abandon under stress.

What to read next

- Spot vs Futures for Beginners

- Manual vs Automated Trading

- Forex Lot Sizing & Risk Management

- What Is OpenClaw?

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. Vanguard 'Dollar-cost averaging just means taking risk later' study; behavioral finance research.