Risk disclosure: Independent research finds 70–84% of Polymarket traders lose money (Sergeenkov, April 2026; Akey et al., SSRN, March 2026). Forex CFDs: 70–85% retail loss rate. Binary options: 80%+ in most jurisdictions. AI agents don't change these baselines. Full disclaimer. Binary options disclosure: CySEC, FCA, and ASIC have all restricted or banned binary options for retail traders in major markets due to consistently high loss rates (typically 80%+). Most binary options brokers operate from offshore jurisdictions with limited consumer protection. We do not recommend binary options as a serious trading strategy for retail capital.

Deriv's synthetic indices are unique in retail trading: markets that don't exist in reality, generated algorithmically, available 24/7. Volatility 75, Boom 1000, Crash 500, Step indices — these are computer-generated price feeds that mimic real market behavior without being tied to any underlying asset. They've become especially popular in SEA, Africa, and Latin America because they're accessible, leverage-friendly, and never close.

This guide explains what synthetic indices actually are, how they work mechanically, why they're popular, the realistic risks (still high loss rate), and how to think about them as an OpenClaw automation target.

TL;DR — The 30-second answer

- Synthetic indices are algorithmically generated price feeds (no real underlying asset).

- Available 24/7 including weekends — major appeal over forex.

- Six main families: Volatility (10-100), Boom/Crash, Jump, Step, Range Break, Drift Switching.

- Deriv loss rate: 71% retail. Better than IQ Option's 83% but still grim.

- OpenClaw integration via official DerivAPI WebSocket. Mature, stable, bot-friendly.

- Why popular in SEA/Africa: low minimum deposit, instant trading, no broker drama.

What synthetic indices actually are

In normal trading, EUR/USD's price reflects real economic flows: importers, exporters, central banks, speculators all transacting. There's an actual underlying market. Synthetic indices have none of that. They're algorithmically generated random price feeds that mimic the statistical properties of real markets without representing any actual asset.

Deriv's algorithm generates a price tick (or candle) every 1-2 seconds for each synthetic index. The algorithm is publicly disclosed by Deriv: pseudo-random number generators seeded by cryptographically verifiable nonces, with each index having different volatility, drift, and jump parameters. The randomness is audited.

This means: there's no "news" that moves the market. No central bank decisions. No economic data. Just a stream of statistically-generated price ticks. For traders, this has interesting implications: you can't have an information edge (no insider knowledge applies), but you can have a statistical edge if your strategy exploits the known mathematical properties of the generators.

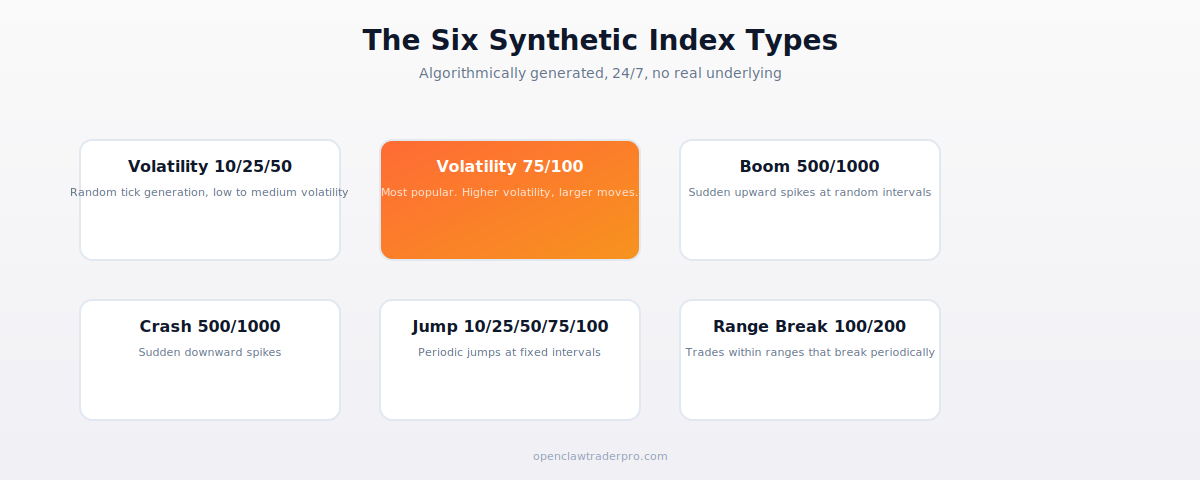

The six synthetic index families

Volatility Indices (10, 25, 50, 75, 100, 250)

The flagship products. The number indicates annualized volatility percentage: Vol 10 moves about 10% per year (very calm), Vol 100 moves about 100% per year (very volatile). Vol 75 is the single most-traded synthetic globally because it's volatile enough for short-term trading but not so wild as to be unmanageable.

Movement style: continuous random walk with normal-ish distribution. No sudden jumps. Behaves like a calm stock or forex pair, just generated by an algorithm.

Boom and Crash (500, 1000)

Boom indices spike upward at random intervals (average every 500 or 1000 ticks). Crash indices spike downward. Between spikes, the price slowly trends in the opposite direction. So Boom 500 trends downward most of the time with occasional sharp upward spikes; Crash 500 trends upward with occasional sharp downward spikes.

Trading style: lots of small losses interspersed with rare big wins (if you're positioned correctly) or one big loss that wipes out many small gains (if you're on the wrong side). Pure martingale strategies blow up regularly on these.

Jump Indices (10, 25, 50, 75, 100)

Periodic jumps at fixed intervals (every 20 minutes on average). Behavior between jumps is similar to volatility indices but with predictable disruption. Some traders try to time the jumps; the official documentation specifically warns that jump timing is not predictable.

Step Index

A single index that moves in equal steps (up or down 0.1 per tick) with equal probability. Pure 50/50 random walk. Used mainly for testing automated systems.

Range Break Indices (100, 200)

Price stays within a range, then "breaks out" up or down at random intervals (every 100 or 200 ticks on average). The breakouts are large and fast. Trade structure encourages straddling or pending orders.

Drift Switching Index

Has slight upward or downward drift that switches direction at random intervals. Less popular but useful for testing trend-following strategies.

Why synthetics are popular (especially in SEA, Africa, LATAM)

Several practical reasons make synthetic indices attractive for retail traders in our audience:

- 24/7 availability including weekends. Forex closes Friday 5pm to Sunday 5pm ET. Crypto trades 24/7 but synthetics have more predictable behavior. For traders with weekend availability (most of us), this matters.

- Low minimum deposit. Deriv allows $5 minimum, with positions sizable from $0.35 per contract. Most forex brokers require $100-500 minimum.

- No news to worry about. EUR/USD spikes 50 pips on NFP release. Vol 75 doesn't react to any news because there's no underlying market.

- Deriv accepts local payment methods. Mobile money (Kenya, Nigeria, Ghana), local banks (Indonesia, Philippines, Vietnam), crypto. Many international brokers don't.

- Mathematical clarity. Strategies can be backtested perfectly because the generator is known. This is unique among retail trading venues.

The honest assessment of profitability

Deriv publishes retail loss data via BVI FSC: 71% of retail traders lose money. This is better than IQ Option's 83% but still grim. The reasons retail loses on synthetics are similar to other markets:

- Most retail traders use martingale or anti-martingale (doubling after wins/losses). Both blow up on Boom/Crash spikes.

- Most retail traders don't understand the statistical properties of the generators. They trade based on chart patterns that work in real markets but not in pure random walks.

- Most retail traders over-leverage. Deriv allows up to 500:1 on synthetics. The math gets ugly fast.

- Most retail traders trade 24/7 because they can. Lack of breaks leads to emotional decisions.

The traders who do profit on synthetics share specific habits: strict 1% position sizing, focused on 1-2 indices (usually Vol 75 + one Boom/Crash), well-defined entry/exit rules in code (not by feel), willingness to step away after 3 losses in a row.

For OpenClaw bot automation

Deriv synthetics are arguably the best target for OpenClaw automation among retail-accessible markets:

- Official API (DerivAPI WebSocket) is mature, stable, well-documented at

developers.deriv.com. - Statistical predictability means strategies can be rigorously backtested.

- 24/7 availability means heartbeat-driven bots work continuously.

- Low minimum trade size ($0.35) makes paper-equivalent live testing affordable.

- Demo mode with $10,000 fake balance lets you test without risk.

The OpenClaw community has built deriv-api skill that wraps the WebSocket API. Setup is described in our Deriv bot setup guide. Realistic expectation: a competent statistical bot on Vol 75 can produce 5-15% monthly returns with proper risk management, but the variance is high and drawdowns of 20-30% are common.

Cautions specific to synthetics

- The generators don't reflect macro reality. Your strategy must work on pure statistical properties, not on "oil prices drove BTC up." Information advantage doesn't exist.

- Past performance is more meaningful than in real markets. Because the generator is stable, backtests are predictive. This is a double-edged sword — you can curve-fit very effectively.

- Boom/Crash spikes are devastating to martingale. A 500-tick downward spike on Boom 500 destroys long positions instantly. Multiple stops needed.

- Deriv can change parameters. They've adjusted volatility settings on synthetics before. Strategies that worked become unprofitable overnight.

- Bot detection. Deriv generally allows automated trading via their API but reserves the right to suspend accounts using browser-automation tools. Use the official API.

📧 Get every new tutorial in your inbox

One email per week. Tutorials, CVE disclosures, broker updates. Unsubscribe in one click.

(Connect FluentCRM / ConvertKit / Beehiiv form here)

Frequently asked questions

Are synthetics legal where I live?

Deriv operates from BVI and is accessible in most jurisdictions except US and a few others. Local laws on derivatives trading still apply — not legal advice.

Is the randomness really random?

Deriv publishes cryptographic verification of the generators. Independent audits have validated their statistical properties. The randomness is real, not rigged in the broker's favor (though the asymmetric payout still means the house has edge).

Can I make a living from synthetic indices?

Documented cases exist of traders making $2K-10K per month consistently. They're rare (the 29% who don't lose, of which a smaller subset profit meaningfully). Most who try lose.

Should I use martingale on synthetics?

No. Martingale eventually catches a sequence that wipes you out. On Boom/Crash specifically, this can happen on a single spike.

Which synthetic should I start with?

Vol 75 is the default for good reason — well-studied behavior, medium volatility, plenty of community strategies to test. Start in demo, focus on one index, master it before adding others.

What to read next

- OpenClaw + Deriv: Bot Setup & Real Expectations

- Binary Options Explained

- Why 80% of Binary Options Traders Lose

- IQ Option vs Pocket Option vs Quotex

Sources cited: The Hacker News (CVE-2026-25253 disclosure, Feb 2026); Conscia 2026 OpenClaw Security Crisis advisory; Snyk ToxicSkills study; Cyber Press ClawHavoc reporting; Wall Street Journal Polymarket profitability analysis (May 2026); Andrey Sergeenkov via The Defiant (April 2026); Akey, Grégoire, Harvie & Martineau, SSRN paper (March 2026); openclaw.ai official advisories; Peter Steinberger public statements on X. Deriv official documentation; BVI FSC disclosures; developers.deriv.com API docs.